I guess I’m supposed to write about the Senate HELP hearing yesterday. I’ve certainly wasted a bunch of pixels in the runup. It would be weird if I ignored it now.

And yet …

I mean, nothing about what transpired was remotely surprising or newsworthy. It was kayfabe (my 2024 Word of the Year), down to pretty much every detail. I didn’t learn anything new about where Bernie stands or how pure populist anger gets translated into policy change.

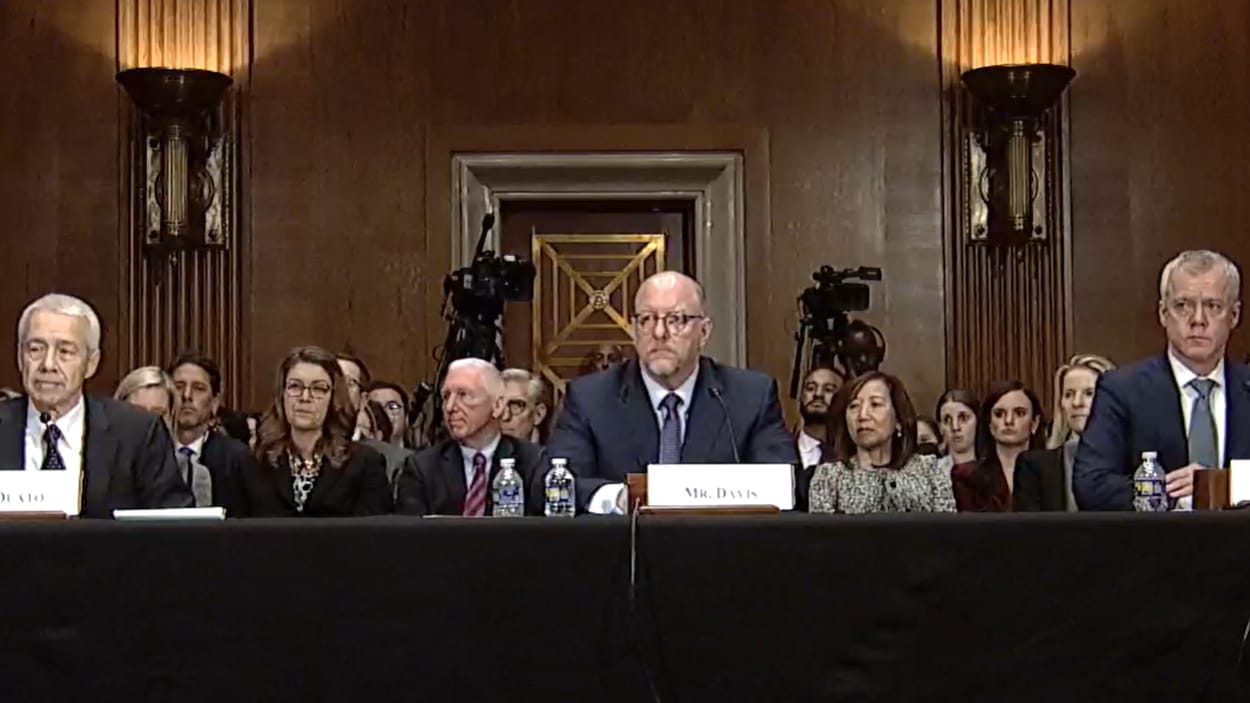

That said, there’s one element worth flagging: two of the CEOs up there, Merck’s Rob Davis and J&J’s Joaquin Duato, offered some fairly explicit net price snippets. Davis said that Januvia’s net price was about 90% lower than list, and Duato said that Stelara’s net was 70% cheaper than the sticker price. (Noteworthy: with the exception of MarketWatch, I saw no coverage of those two nuggets.)

I hadn’t heard those disclosures before (please correct me if I missed ‘em), and they’re very small steps in the right direction on transparency. Because if we’re going to have a sensible discussion on price, we’re going to need to use net prices**. Otherwise, we’ll just end up talking past each other.

(For more on “talking past each other,” NPC’s John O’Brien posted a strong piece on LinkedIn yesterday.)

** To be clear, list prices are not unimportant, especially when it comes to coinsurance and the uninsured. So let me amend slightly: not only would be it good if we had and used more net price data, it would be even better — both for me and for the pharma industry — if that list-to-net bubble was popped entirely.

It’s useful to think about the prices CMS is going to affix to the 10 medicines selected for price controls in two different ways.

First, we need to find out if a given price SOUNDS BAD for pharma. In other words, can you create a really dramatic-sounding headline based on the price? And then we need to determine if the price is ACTUALLY BAD in a way that will hurt the company, damage innovation, etc.

It’s possible to have a price that SOUNDS BAD but is ACTUALLY OK. Indeed, if Januvia is already being sold at a net price that is 90% below its list price, this scenario feels likely.

The opposite is also possible, though a SOUNDS OK, ACTUALLY BAD scenario is unlikely outside of Imbruvica, for reasons I talked about earlier in the week. And, of course, there is always the possibility of SOUNDS BAD, ACTUALLY BAD.

So I’ve plotted those options in a classic 2×2 matrix, above. My theory is that anything above the red line is a win for the government. They don’t need to be in the upper right corner and disrupt the whole pharma marketplace. They just need to show dramatically lower prices. (There’s a whole other set of conversations about popping the list-to-net bubble and formulary design that impact prices above the red line, but I’ll ignore all of that today.)

And industry wants to stay to the left of the blue line, obvs.

So the big parlor game of the next six months will be guessing which quadrant each one of the 10 prices will fall in based on corporate body language and the like.

And we haven’t gotten much corporate body language. At least, not before yesterday, when AstraZeneca CEO Pascal Soriot told reporters he was “relatively encouraged” by the initial offer that the company received, presumably for its Farxiga medicine.

Endpoints’ Drew Armstrong noted that “relatively” was an important word there, and that the statement shouldn’t be seen as a sigh of relief. But “relatively encouraging” seems like a great way to describe the upper left quadrant of SOUNDS BAD, ACTUALLY OK.

There’s no way of knowing for sure before Sept. 1, but I like the guessing games.

This is quite the exchange.

Yesterday, I mentioned that the New York Times had repeated a puzzlingly bad line: “In the United States, negotiations over drug prices are fragmented across tens of thousands of health plans and employers.”

Adam Fein over at Drug Channels noticed, too, putting out a tweet highlighting that absurdity. The NYT reporter Rebecca Robbins replied, doubling down (and probably violating the First Law of Holes): “PBMs don’t negotiate one single price for all of their employer and health plan clients.”

That prompted Mark Cuban to get involved: “The system isn’t fragmented. The PBMs take advantage of their customers. That’s it entirely.”

Elsewhere:

I still have no idea if the lawsuit accusing J&J of accepting a health plan so bad that it violated their fiduciary duty to employers holds water, but Bloomberg Law predicted that the legal action is likely to spur more, similar complaints.

What I do know is that the J&J suit is already being weaponized in other ways. The Mark Cuban Cost Plus Drug Company put this post on LinkedIn yesterday highlighting the difference between the MCCPDC cost and “What You May Be Paying.” The “What You May Be Paying” numbers came straight from details in the lawsuit, which was a fascinating (and quick!) move from Cuban’s folks.

The mechanics of the new IRA-enable “smoothing” mechanism, in which a Medicare beneficiary can spread their medicine costs over the course of the year rather than getting slammed in January, are detailed well in this new Health Affairs Forefront piece. The analysis deconstructs a not-particularly-unlikely set of circumstances in which smoothing could lead, ironically, to surprisingly large bills.

If this email was forwarded to you, and you’d like to become a reader, click here to see back issues of Cost Curve and subscribe to the newsletter.